By Julian Gary

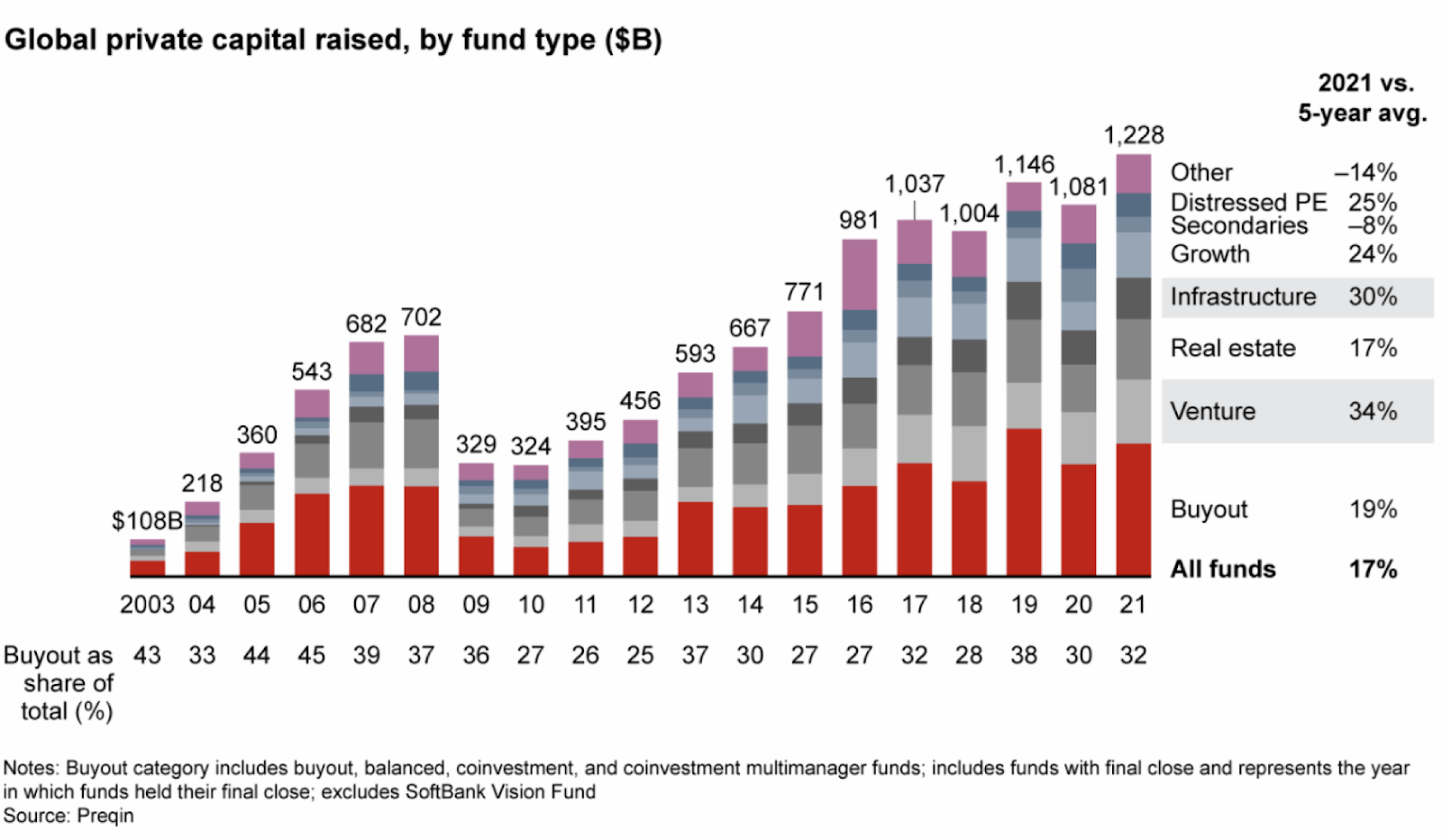

In the past two decades, institutional investment in private equity funds has skyrocketed. According to Bain & Company, Global Private Equity funds raised $1.2 trillion in 2020, up from $108 billion in 2003.

The rapid rise in funding, as well as criticism from Congress regarding the employment effects of private equity ownership, has brought scrutiny to the asset class’s supposed outperformance. Skeptics have cited that the fund’s returns barely beat public markets, thus begging the question, why have institutional dollars continued to be poured into private equity, and is this investment justified? This article will present a neutral analysis of this question.

Investors have been drawn to the asset class by promises of market-beating returns as well as a lack of correlation with the overall market. On the surface, this seems to be true. According to the McKinsey Private Markets Report, in 2021, private equity was the highest performing asset class in the private markets for the fifth consecutive year.

Furthermore, private equity firms boast of low volatility and returns uncorrelated with the broader market. From 1994 to 2017, the Cambridge Associate Private Equity Index registered volatility half of that of the S&P and lower than the 10 year treasury. The same data also shows negative correlation between annual private equity IRRs and the S&P, supporting alleged diversification benefits of the asset class.

However, critics have questioned the accuracy of these figures and the potential for private equity returns to continue their outperformance. With respect to accuracy, private equity returns data are not truly comparable to the returns of the public market. In private equity, returns are measured based on IRR, which is a measure based on actual cash distribution to investors rather than current market values of the underlying assets. In contrast, public market securities can be valued daily. Research continues to use IRR as a measure simply due to the lack of comparable metrics. Up-to-date returns measuring is also complicated by the fact that private equity investments are inherently hard to value unlike public equities. While private equity firms will give updated valuations of their portfolio companies every quarter, these valuations are subjective and involve a high degree of discretion on the part of the general partner. As such, private equity returns are often subject to “smoothing,” where valuations are overstated in bad times, and potentially understated in good times. The effect of smoothing may be a cause of the outperformance of private equity firms during economic turmoil. For example, in 2008, private equity firms registered IRRs of 11% while the S&P 500 fell 38%. Despite returns smoothing’s potential to be misleading, it may also offer real counter-cyclical benefits by protecting investors from acting irrationally based on temporary, on-paper losses.

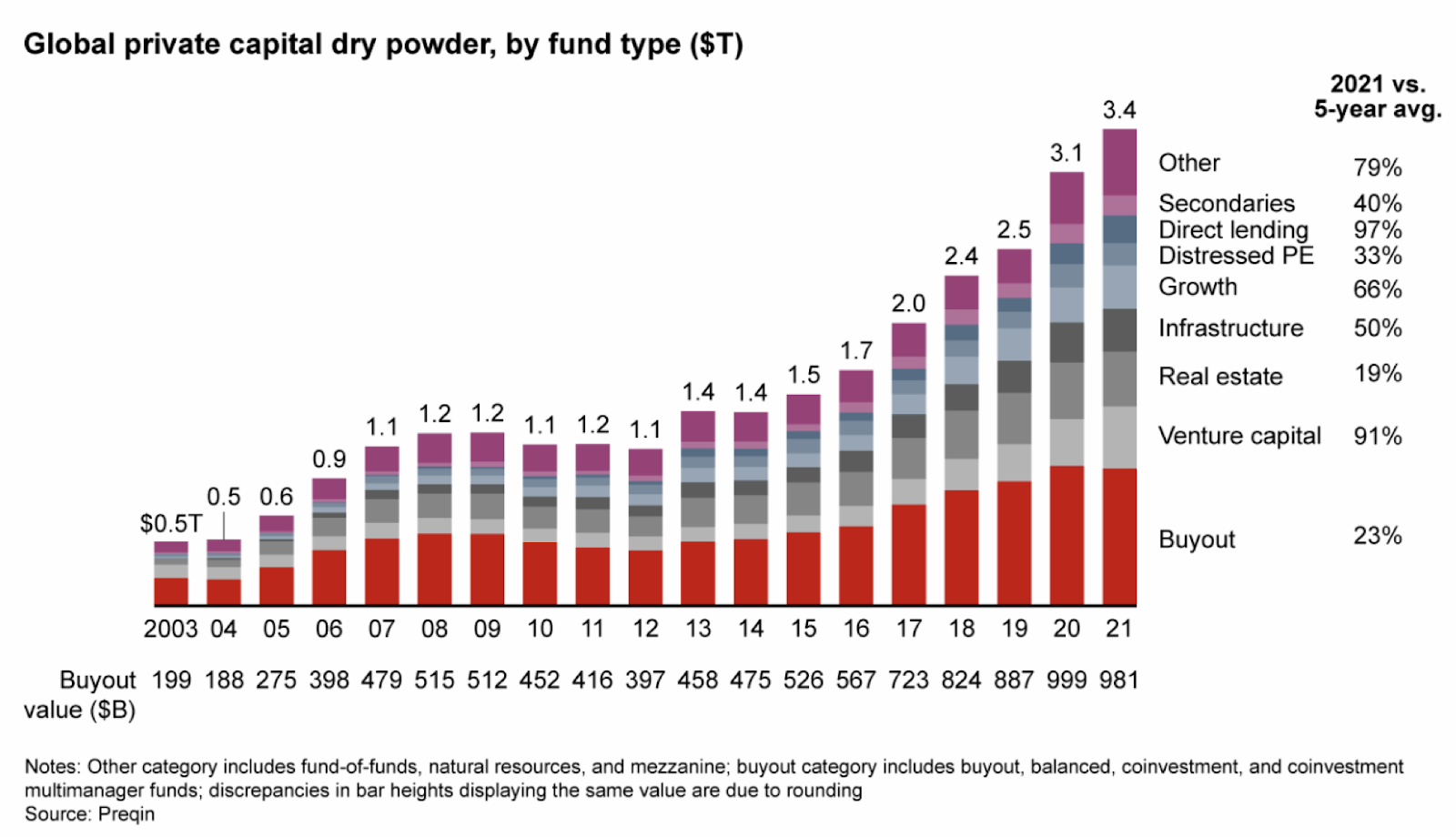

Regarding private equity’s supposed outperformance, in the past decade, private equity returns over market returns have been narrowing. From 1990 to 2010, private equity firms outperformed the S&P by 6.3%, net of fees. However, according to the American Investment Council, in the decade preceding September 2020, private equity funds generated a 14.2% median annualized return compared to annualized return of 13.7% for the S&P 500. The diminishing incremental returns can partly be attributed to the increasing amount of competition in the industry. As investors allocate a larger and larger percentage of their portfolios to private equity, attractive investment opportunities have become harder to come by. This is evidenced by the drastic increase in “dry powder,” or the capital committed by investors that has not been used to make investments in target companies. From 2003 to 2021, private market dry powder increased by 580%, going from $500 billion to $3.4 trillion.

The increased competition may hamper future returns due to lack of attractive opportunities, as well as the high multiples demanded by sellers. In a 2018 report, the Head of Global Macro at KKR noted these trends and expects returns to decline while remaining attractive on a risk-adjusted return basis.

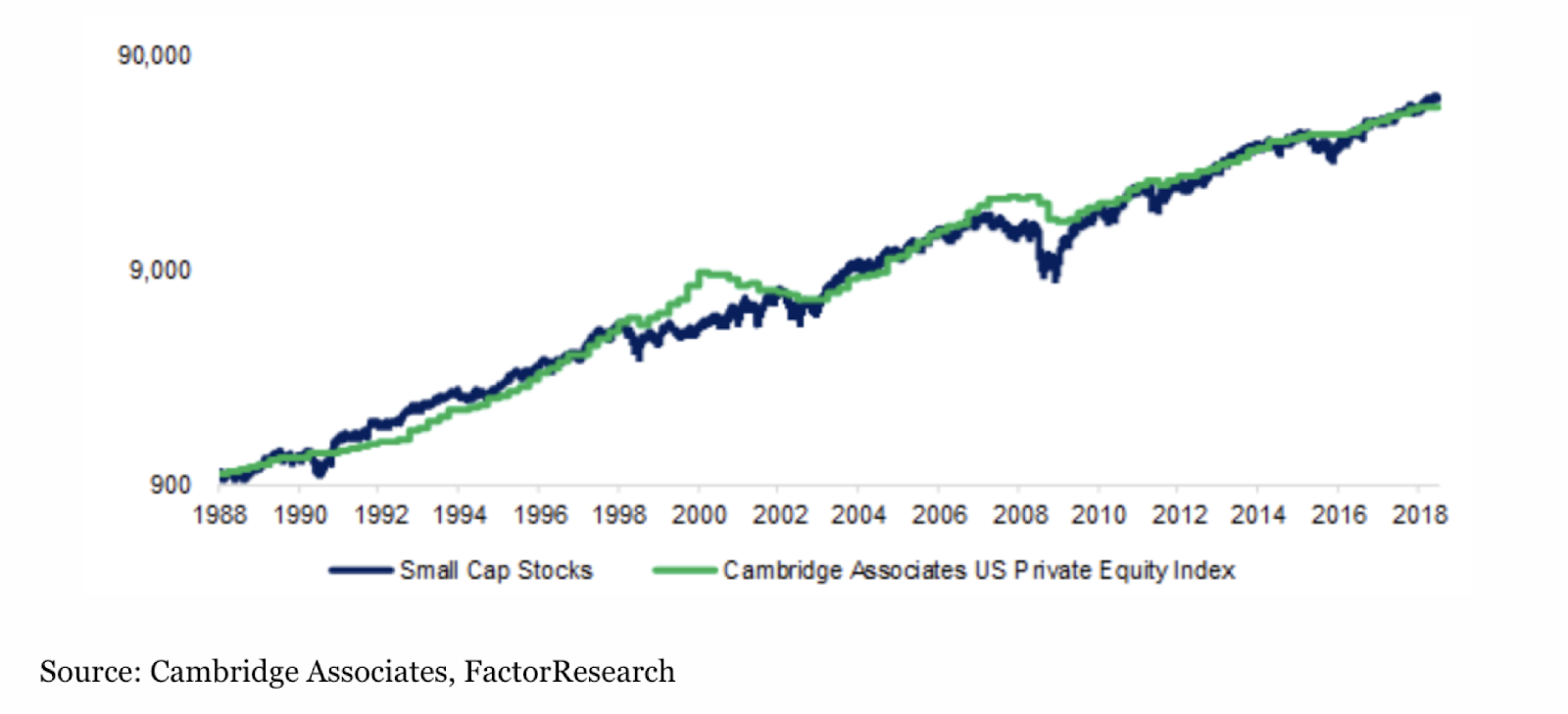

Critics have further postulated that because most private equity deals are comparable in size to small-cap companies, private equity returns can be replicated through a small-cap stock portfolio. To test this hypothesis, Nicolas Rabener, a writer for the CFA Institute, compared an index of the smallest 30% of U.S public companies with a market cap greater than $500m to private equity returns. His results are presented in the graph below.

Despite the negative correlation between private equity annualized returns and the S&P 500, the correlation between the constructed small-cap index and private equity returns was .74, suggesting limited diversification benefits. While the study may appear to challenge the necessity of private equity, it’s important to note that investment managers choose funds individually rather than on an aggregated basis. Within private equity, there’s a large array of fund types, including growth equity, large-cap buyout, distressed, and venture capital. Managers choose allocations depending on the perceived diversification benefits and expected returns of each individual fund and the fund class. Furthermore, successful general partners can make value-added improvements within their portfolio companies as well as provide liquidity. A study by Alex Belyakov of The Wharton School found that UK private equity-backed companies responded better to financial distress, and thus concluded private equity returns couldn’t be replicated by the public markets.

Private equity’s momentum has remained strong into 2022. Thus, despite the skeptics, institutional investors clearly still see the asset class as attractive on a risk return basis. In the coming year, higher interest rates are likely to put downward pressure on LBO deal activity. However, private equity has proven itself to be resistant in downturns, which may drive additional investor allocations to the asset class if markets experience distress. □

Leave a Reply