Image Source: Pixabay

An economic analysis of why rational GMs keep signing irrational-looking contracts and how to redesign their incentives considering risk allocation, cap convexity, and distorted investments

By: Advait Sunil

Edited by: Zane Govindraj

It’s a scene so iconic you could recognize it even if you’ve never followed a sport in your life. A general manager grinning beside a newly signed superstar, cameras flashing as the jersey goes up. Behind that photo-op sits an enormous contract that is almost certainly back-loaded. Interest in tickets rises, local media proclaims a new era, and fans convince themselves their team has taken a decisive step toward contention for a title. For the General Manager, the move already looks like a win, long before the later, riskier years of the deal arrive. The most straightforward economic explanation for these moves is that teams function as firms: players’ marginal revenue product can be modeled as value, and their revenues flow from media, sponsors and tickets. Furthermore,their payrolls and bargaining power are shaped by how demand responds to price or superstar presence, as well as salary caps that act as financial guardrails.

Figure 1: We can compare real annual payment structures from Shohei Ohtani’s (back-loaded) and Juan Soto’s (front-loaded) Major League Baseball contracts. Ohtani receives only $2M annually through 2033, with $68M deferred to 2034–2043. Soto, by contrast, receives a $75M signing bonus and over $46M annually in the first several seasons, illustrating how risk can be deferred or preponed in contract design.

Source: Sporting News and AP News

But that view leaves out something critical. “The team” is not a stereotypical single, unified decision-maker. The tug-of-war between owners’ equity expectations, the GM’s incentives, and legal or financial constraints rarely enter the frame. Hence, we can’t assume that clubs act as rational “firms” in trying to maximize long-run value. Real front offices behave as overlapping agents with conflicting objectives: executives whose compensation is heavily front-loaded into the next season or two will behave as if they hyperbolically discount long-term sustainability. In Cornell’s Einaudi Center for International Studies’s article “Convexity and Short-Termism in Banker Compensation”, Jacob Fisher argues, “Short-termism arises when an investment strategy has positive expected value over a short time frame, but because of large long-term risks, it has a negative expected value overall… and if the risks taken because of short-termism are large enough… the downside will also fall on the investor… so oversight committees also pay attention to short-termism.” This is not suggesting in the slightest GMs are reckless or irrational. Instead, guarantees, buyouts, no-trade clauses, and injury protections – products of Collective Bargaining Agreements and contract law – create an internal friction between the GM’s privately optimal and rational choice and the owner’s long-run investment targets. Duane Rockerbie’s “The Economics of Professional Sports” underscored that “At the level of the professional sports league, we assume that club owners set ticket prices to maximize economic profit and net present value.” So what fans criticize are not just “bad” deals, but a classic principal-agent problem in a failure of incentive design.

Image Source: The Legal Implications of Executive Compensation Packages

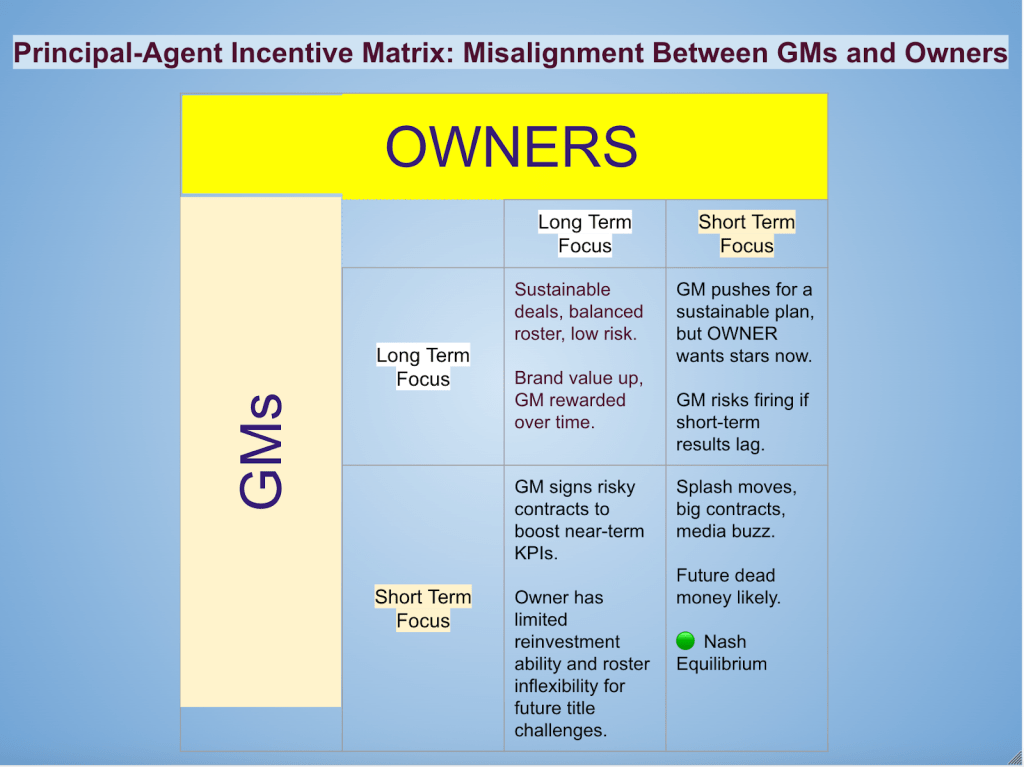

Figure 2: The vertical axis reflects the GM’s time horizon (long-term vs. short-term focus), while the horizontal axis reflects the owner’s investment horizon. When both focus long-term, optimization occurs. But when incentives diverge or both economic actors pursue short-term gains, financial inefficiencies emerge. The bottom-right cell reflects the common Nash equilibrium: stable, but suboptimal for long-run team value.

To understand why the system produces bad contracts, we need to first understand how the structural institutions that dominate American sports markets ask its decision-makers to behave. It’s no secret salary caps in today’s major leagues are rising rapidly. The National Basketball Association is projected to climb over 10% allowed for the previous season, while the National Football League expects its cap to reach at least $277.5 million per team. At first glance, this might seem beneficial for owners, since it works like an annual increase in a team’s production frontier; why not just “produce” more wins by purchasing more or better labor? After all, the presence of superstars can push parts of the demand curve into a quasi-luxury regime: certain fan segments become markedly less price sensitive, paying more to see signature players. But as you might expect, this analogy is quite misleading, because win production is almost never determined by a single-period resource choice like labor. Sports are played on the playing field, and aren’t automatized like technology. Moreover, they have no substitutes, as no athlete can truly replace another in terms of skill sets and abilities. “Socioeconomics of Sport”, a book published in 2023 by Jean-François Bourg and Jean-Jacques Gouguet, points out how “this reputational capital confers on its holder a quasi-rent (the surplus linked to the superstars’ advantageous position). This is especially true since the pleasure or utility of consuming the superstars’ services escapes the law of diminishing marginal utility instead of causing a gradual saturation.” Even outside of the playing field, their looks and the values associated with them — prestige, luxury, success and hard work — incentivize higher wages and for these stars to absorb a disproportionate share of the cap, contributing to a more polarized wage distribution. The result is an arms-race Nash equilibrium: overpaying may be individually rational given others’ behavior, even though all would be better off not overspending. Additionally, owners are unsure if players will take advantage of no-trade clauses and buyout provisions, running the risk of a negative return on investment. This asymmetric information also worsens loss aversion, because if one team signs a star, others fear being left behind competitively, as well as commercially with fans.

Figure 3: We can see how in the NFL, approximately 57% of a player’s contract value is guaranteed, meaning teams are obligated to pay this portion regardless of performance or release. The remaining 43% is typically non-guaranteed, exposing players to financial risk if they are cut or injured (having somewhat of a balance).

Figure 4: Unlike in the NFL however, NBA contracts are generally fully guaranteed, requiring teams to pay out the full contract amount even if a player is released. This places nearly all financial risk on owners, with players facing minimal contractual downside once a deal is signed, with a 5-10% portion excluded after malus/clawback deductions.

Source: ESPN

Be that as it may, once property rights over labor and performance are defined by contract law and CBAs, economics naturally focuses on how those rights allocate risk between players and clubs. This defines the shape of that future cost curve for the club, as legally binding commitments. Guarantees, for example, shift nearly all downside risk cost onto owners, despite a lack of information from the owner’s perspective on whether performance or fitness will sustain.

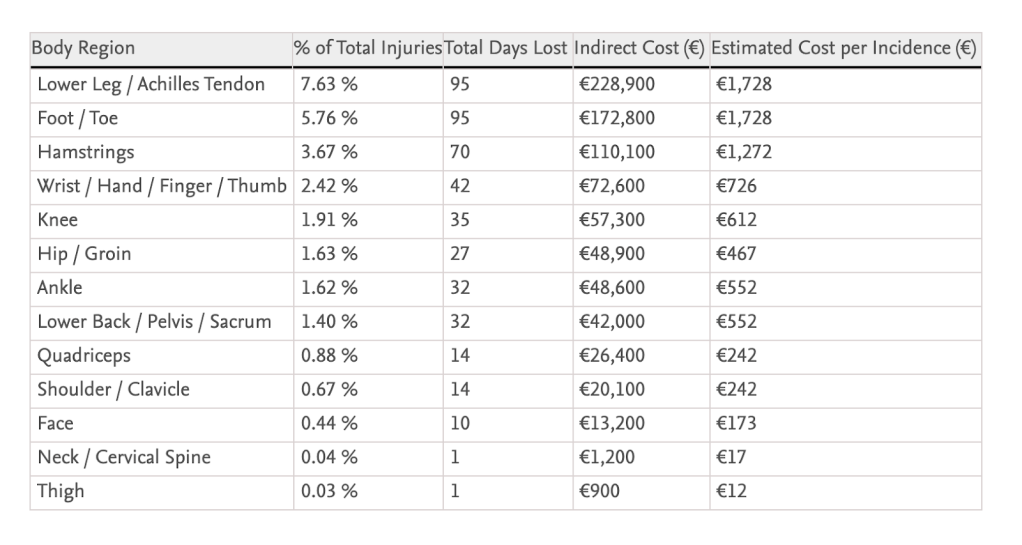

Figure 5: We can see the distribution of injury types by frequency, days lost, and indirect cost. Lower leg and foot/toe injuries are the most common and costly, each averaging over €1,700 per incident.

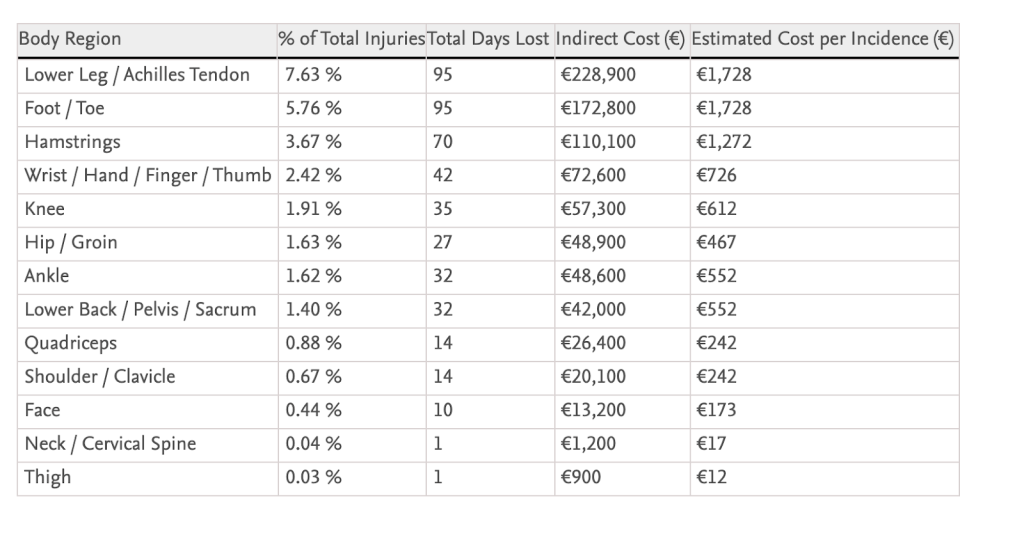

Figure 6: Similarly, data collected also extended to injury categories by average cost per occurrence, showing hamstrings and lower leg injuries drive high per-incident costs, reinforcing their role in long-term financial risk for teams.

Source: Apunts Sports Medicine

As customary to contract law, there is some scope for injury protection and contract-termination within American sports leagues that determine who bears performance and medical risk over the life of a deal, though it naturally differs from league to league. For example, a recent high-profile dispute between the Las Vegas Raiders and Christian Wilkins – a key defensive player in the NFL signed to a long-term contract – over injury guarantees illustrates how aggressively teams defend these clauses once injuries intervene.

In this case, the Raiders tried to void protections meant to shield the player from exactly those risks, which shows how these economic agreements can quickly become disputed financial obligations as soon as performance or health comes into question. So owners are basically left with “dead money” (funds tied up in unprofitable investments), which is a sunk cost that essentially reduces their ability to reallocate resources efficiently in future seasons. This ultimately appears as an impairment charge on the teams’ balance sheets, which drastically raises the teams’ costs.

Unlike the owners, though, GMs’ incentives tend to rest on short-run key performance indicators, such as year-to-year win totals, playoff appearances, attendance, local buzz, etc. However, in ensuring they maximize their compensation, they often fail to incorporate long-run risk, as they naturally orient toward immediate gains. This gap helps explain why some deals that look inefficient later were fully rational from a GM’s perspective at the time. Studies of MLB’s post-pandemic demand by Soojin Choi, Fang Zheng, and Seung-Man Lee of the Multidisciplinary Digital Publishing Institute showed that when fans believe their team is competitive and emotionally attached, loyalty rises and consumers of stadium tickets become less price sensitive. Similar dynamics exist across leagues: star acquisitions and “win-now” short-term narratives strengthen teams’ bargaining positions with sponsors and broadcasters ex ante, allowing higher markups in the short run. Consequently, a major signing shifts a franchise into a more inelastic demand range almost immediately, even if it looks inefficient ex post.

Similar to housing markets, the sports industry is also tiered into several pricing segments. At the top are products that behave like luxury goods, where higher prices can increase demand (e.g: signature athlete lines). Conversely, at the lower end, there are inferior goods, such as cheap knockoff jerseys. Even if the seating capacity is perfectly price-inelastic due to the fixed quantity of seats, we can assume producer surplus and owner revenue would increase through increase in demand owing to the superstar signing(s). In fact, the short run, for the team, may even exceed all expectations for consumer and producer surplus. Higher attendance and streaming subscriptions to see the highest statistically rated players, coupled with higher ticket prices, would justify the big contracts. However, sports are almost never linear, since the GM tends to get fired in the medium term when success dries up. If the fans and owners do not back their managers, this could cause a downward spiral, where the team gets stuck in partial rebuilds, with limited pricing power and heavy sunk costs.

Even one of the most marquee franchises in basketball, the Los Angeles Lakers — tied for the most championships, numerous Hall of Famers, and the record of the longest winning streak — face consequences from this salary cap purgatory. This actually even functions like restricted choice architecture for NBA franchises. Even before buying one of the league’s superstar defenders, Marcus Smart, they already had two of the most famous stars in Lebron James and Luka Dončić. The Lakers have tried to improve this year, but they currently don’t have enough room below the hard cap to sign anyone to even a veteran-minimum contract. So they have almost exclusively operated through draft picks and two-ways supporting the idea that they are stuck trying to build depth and a functional roster, but under heavy financial or structural constraints. This prevents them from adding any new players who would meaningfully raise their overall talent level, which even the most talented of rosters need to increase revenue, mostly by competing for the championship and raising media value.

We already have the blueprint to meet owners’ multi-period net present value, while preserving flexibility for justified risk-taking. The Boston Scientific Investor’s corporate governance charter, adopted in 2025, stresses that incentive plans should include malus or clawback features to address excessive risk-taking and misaligned pay. For context, a “clawback” or “malus” provision enables a company to recover previously paid compensation or trigger forfeiture of unpaid compensation. Though we know most sports teams would economically budget some allowance for dead money and contract risk exposure, particularly towards aging or injury-prone players), the owners should ensure that a fixed share — say, 20-30% — of GM variable pay be deferred and made contingent on meeting long-term sustainability targets. After all, GMs cannot be part of labor since there is conflict of interest. Instead, they represent employer interests such as hiring, firing and negotiating. As a result, the deferred share ensures they would not be able to focus on short-term compensation alone, as any aggressive, short-sighted decisions, would result in a part of that deferred pool being forfeited or reduced. Such a multi-year performance evaluation, alongside weighing multiple-year win percentage, roster age and depth balance, and injury-adjusted value retained (using metrics informed by 2025 injury-cost research by the National Library of Medicine), would shift the questions from “did we win this year?” to “did we build a resilient and economically sustainable portfolio of contracts and talent over several seasons?” The effects could be realized immediately from day one, with the most extreme back-loaded, high-risk contracts being reduced. While there will always be asymmetric information about how much latitude should be granted for aggressive roster decisions, history shows that (driven in part by hyperbolic discounting), without deferred and contingent incentives, teams systematically overuse that latitude over the medium term. As a result, dead money accumulates, crippling the team financially, and increasing the likelihood of boom-and-bust cycles for fans.

Beyond sports, this principal-agent problem speaks to a broader theme in economics and corporate law, when agents make distorted investment decisions under present bias quite predictably. So governance mechanisms must explicitly internalize long-run consequences for the GMs themselves. The core message is simple: to fix “bad” contracts, we need to fix the incentive system that creates them.

Leave a comment